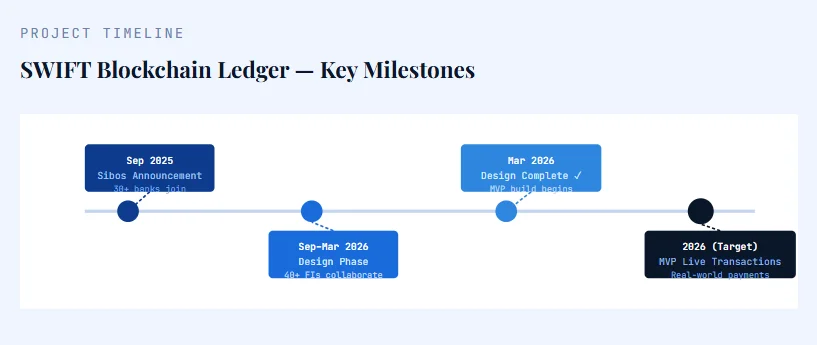

April 03, 2026 – The messaging giant has completed its design phase. It now enters active build mode with 40+ global banks. This is the biggest infrastructure upgrade in cross-border payments in decades.

In Summary

SWIFT completed the design phase of its blockchain shared ledger in March 2026.

The MVP is built on Hyperledger Besu, an EVM-compatible, open-source platform.

Over 40 banks are actively involved in building and testing the system.

Live cross-border transactions using tokenised deposits will begin in 2026.

The G-10 central banks and the ECB provide regulatory oversight.

SWIFT has officially moved into the build phase of its blockchain-based shared ledger. The network confirmed that the design phase is complete. Now, SWIFT is actively building a minimum viable product (MVP). Participating banks will begin live transactions before the end of 2026.

Indeed, this marks a pivotal moment for global finance. SWIFT connects over 11,500 institutions across 200+ countries. The network also manages more than 40,000 active payment routes. Adding a shared digital ledger fundamentally changes SWIFT’s role, from messaging about money to actually moving it.

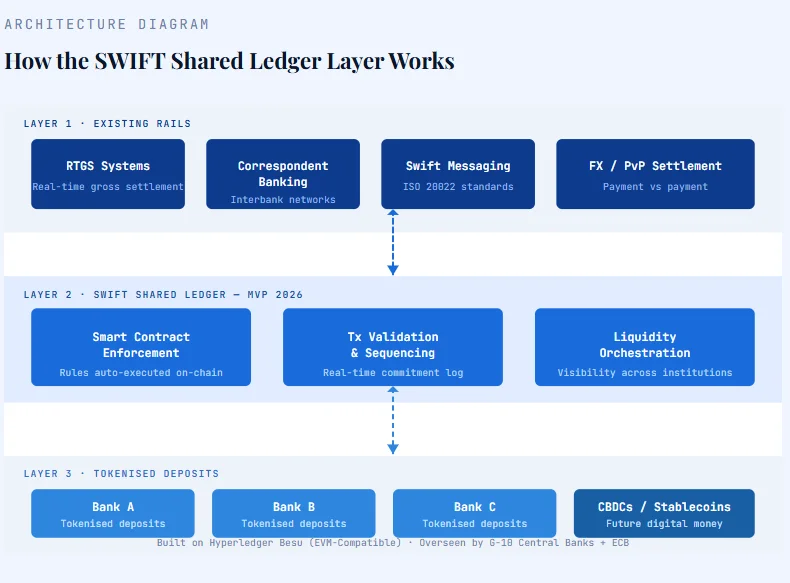

What Is the Ledger, Exactly?

The ledger is a shared digital orchestration layer. Specifically, the system records and validates interbank payment commitments in real time. Furthermore, banks can execute 24/7 cross-border payments using tokenised deposits. Crucially, the ledger does not replace existing settlement rails. Instead, it sits alongside RTGS systems and correspondent banking relationships.

SWIFT operates the ledger. However, banks retain full control. Each institution manages its own keys, assets, funding, and settlement mechanisms. Notably, this architecture is deliberately non-disruptive. Rather than competing with parallel rails, the design enhances existing infrastructure.

The technology stack is open-source and EVM-compatible. Specifically, SWIFT built the MVP on Hyperledger Besu. As a result, the system integrates with the broader Ethereum ecosystem. Consequently, banks gain future interoperability with CBDCs, stablecoins, and digital assets.

“You may think: aren’t those opposites? Swift and blockchain. TradFi and DeFi. In the regulated system of the future, we believe they can go together.”— Javier Perez-Tasso, CEO, SWIFT

Who Is Involved?

The coalition includes more than 40 global financial institutions. Notable participants include Wells Fargo, ANZ, Bank of America, BBVA, and UOB. SWIFT first announced the initiative at Sibos 2025 in Frankfurt on September 29, 2025. Since then, the design phase consumed roughly five months of collaborative work.

Why This Matters for Global Finance

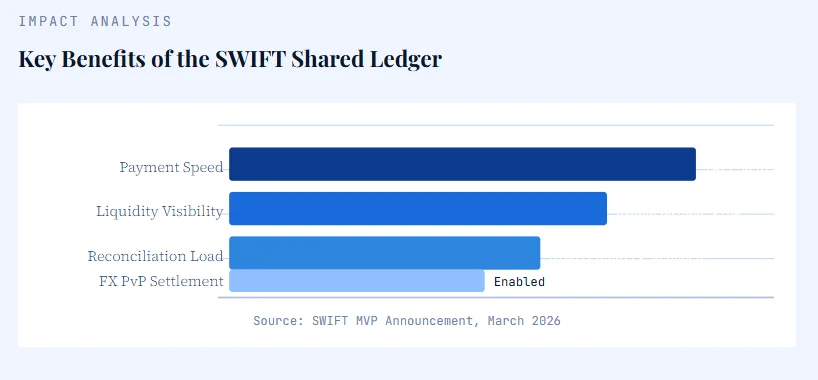

Cross-border payments remain slow, costly, and fragmented. The current system relies on correspondent banking networks built decades ago. Clearly, SWIFT’s ledger targets three critical pain points. Accordingly, it promises faster execution, better liquidity visibility, and reduced reconciliation between banks.

Beyond payments, the ledger unlocks advanced use cases. These include programmable corporate payment flows and foreign exchange payment-versus-payment (PvP) settlement. Moreover, banks can coordinate cash flows associated with securities transactions. Together, these capabilities build a foundation for an entirely new digital payments stack.

Regulatory Oversight and Trust

This initiative operates within a clear regulatory framework. Specifically, the G-10 central banks and the European Central Bank provide formal oversight. The National Bank of Belgium serves as the lead overseer. Importantly, the system requires no new rulemaking. SWIFT also embeds existing compliance processes, including AML and sanctions screening, directly into its architecture.

Additionally, more than 25 banks will introduce SWIFT’s new retail transaction framework by the end of June 2026. This runs in parallel with the ledger initiative. SWIFT describes this dual approach as its “parallel track strategy”, upgrading existing rails while simultaneously building new digital ones.

The Bottom Line

SWIFT is not disrupting global finance. Rather, it is digitising it, carefully, at scale, with regulators at the table. The tokenised deposit ledger represents the first concrete step. When the MVP goes live in 2026, the network will mark a shift from messaging about money to actually moving it. Ultimately, for 11,500 institutions across 200 countries, that shift cannot come soon enough.