March 30, 2026 – The once-booming shadow lending market faces its first major liquidity crisis. Rising defaults, AI disruption fears and a wave of fund redemptions are reshaping the sector in 2026.

In Summary

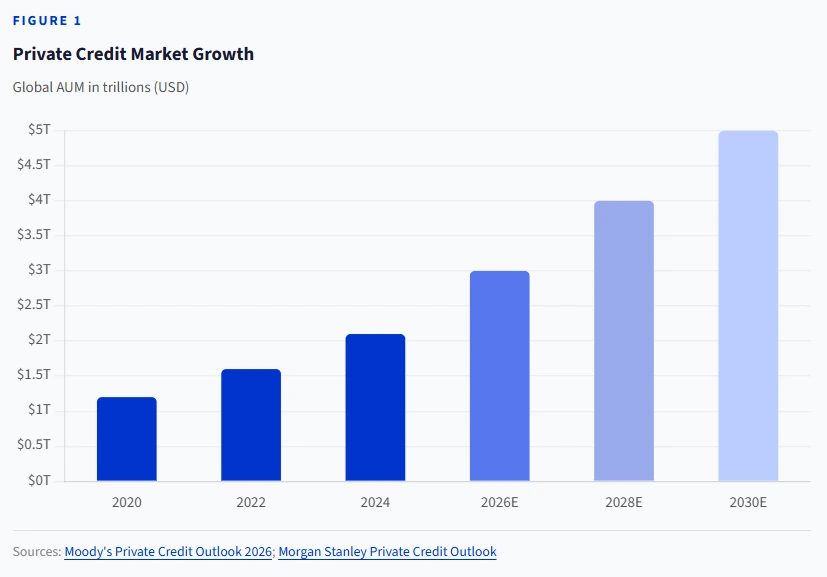

Private credit has grown to roughly $3 trillion globally.

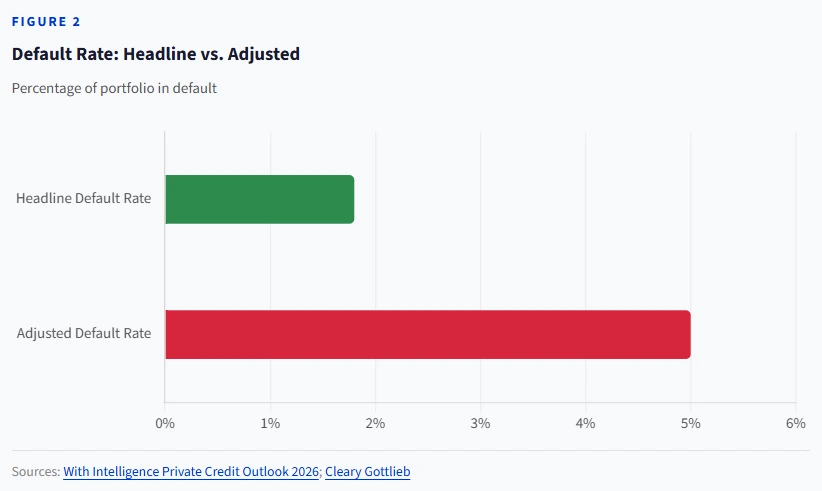

The headline default rate is below 2%, but the adjusted rate is near 5%.

Major funds from Ares, Apollo and Blue Owl have capped redemptions.

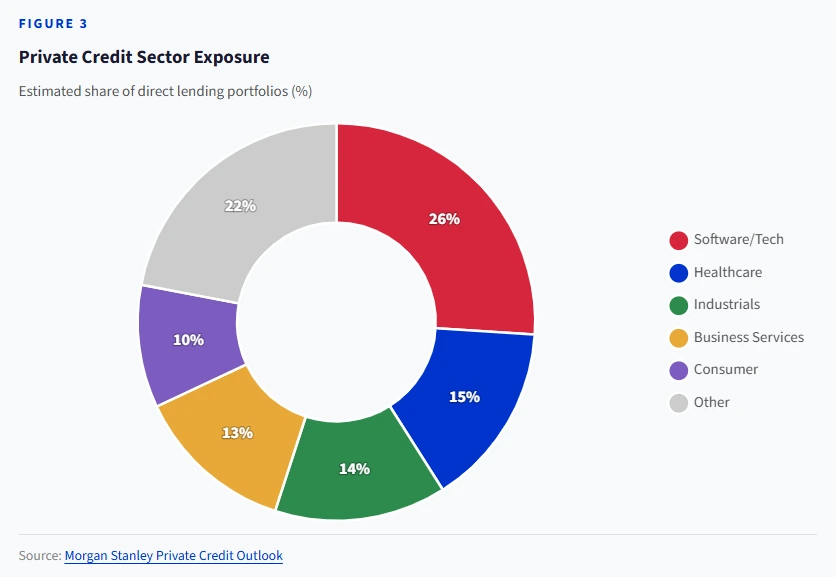

Software exposure in direct lending is estimated at 26%.

Moody’s projects the market could hit $4 trillion by 2030.

Private credit entered 2026 riding a decade-long boom. The sector now rivals the leveraged-loan market in size. But cracks are widening fast.

Investor withdrawals, rising loan defaults and questions about asset quality have rattled the $3 trillion sector. Several of the industry’s biggest names have restricted redemptions. The mood has shifted from euphoria to caution.

A Liquidity Test Like No Other

Ares Management capped withdrawals from its $10.7 billion fund at 5%. Requests had surged to 11.6%. Apollo imposed similar limits on one of its vehicles. Blue Owl Capital blocked retail investors entirely from one of its funds.

Nicolas Roth of UBP called this the first real liquidity test for private credit at scale. Default rates are elevated but manageable, he noted. However, redemption pressure and slowing deal flow are hitting simultaneously.

“The adjustment period will separate strong platforms from weak ones relying on subscription momentum.”— Nicolas Roth, Head of Private Markets Advisory, UBP

Shadow Defaults Tell the Real Story

The headline default rate in private credit has stayed below 2% for years. That figure is misleading. Once selective defaults and restructuring exercises are included, the adjusted rate approaches 5%.

Use of payment-in-kind (PIK) interest has also climbed steadily. Public BDCs now receive about 8% of income via PIK. This masks stress by deferring cash payments.

Lincoln International analysed 7,000 company valuations across 225 managers. It found that enterprise values grew modestly. But EBITDA growth among borrowers is declining as lower-quality deals flood the market.

AI Disruption Adds a New Layer of Risk

Software companies make up the largest sector exposure in private credit. Morgan Stanley estimates direct lending’s software allocation at roughly 26%. Apollo’s Debt Solutions BDC holds over 12% in software alone.

Fears that agentic AI could disrupt the SaaS business model sent public SaaS stocks tumbling. The contagion has spread into private markets. Lenders concentrated in tech-heavy portfolios now face the sharpest scrutiny.

At the same time, AI is creating new opportunities. Morgan Stanley projects private credit could fund more than half the $1.5 trillion needed for global data-centre buildouts through 2028.

Growth Is Not Over, But the Rules Have Changed

Despite the turbulence, the asset class continues to expand. Moody’s forecasts AUM exceeding $2 trillion in 2026 alone. The market could approach $4 trillion by 2030 and $5 trillion by 2029, per Morgan Stanley.

Fundraising remains robust. Over $165 billion flowed into private credit in 2025. About $95 billion is targeted for direct lending. The U.S. also opened the $13 trillion defined-contribution market to private credit managers for the first time.

Speciality finance is emerging as a rival to direct lending. In the first three quarters of 2025, speciality launches outnumbered direct lending launches 84 to 71. Asset-based finance could eventually overtake direct lending as banks continue de-risking.

The Bottom Line

Private credit is no longer a niche strategy. It is a core pillar of global finance. But the era of low defaults and easy returns is ending. Managers who relied on loose covenants and subscription-driven liquidity face a reckoning.

For disciplined investors, this shakeout may create opportunity. Distressed and opportunistic funds have raised over $100 billion in the past two years. They are now positioned to deploy that capital into stressed assets.

The message for 2026 is clear. Private does not mean protected. And the sector’s first real credit cycle will separate the survivors from the casualties.