March 27, 2026 – Borrowers can now pledge Bitcoin or USDC as collateral for a Fannie-backed home loan, but a steep volatility haircut reshapes the math.

In Summary

Fannie Mae now backs crypto-collateralised mortgages via Coinbase and Better Home & Finance.

Borrowers pledge Bitcoin or USDC instead of cash, avoiding capital gains taxes.

Interest rates run 0.5–1.5 percentage points above standard 30-year mortgage rates.

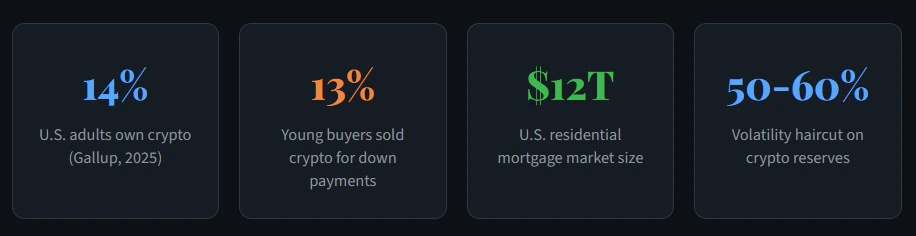

A 50–60% volatility haircut means $100K in Bitcoin counts as only $40K–$50K in reserves.

The FHFA directive from June 2025 made this possible, aligning with the Trump administration’s pro-crypto agenda.

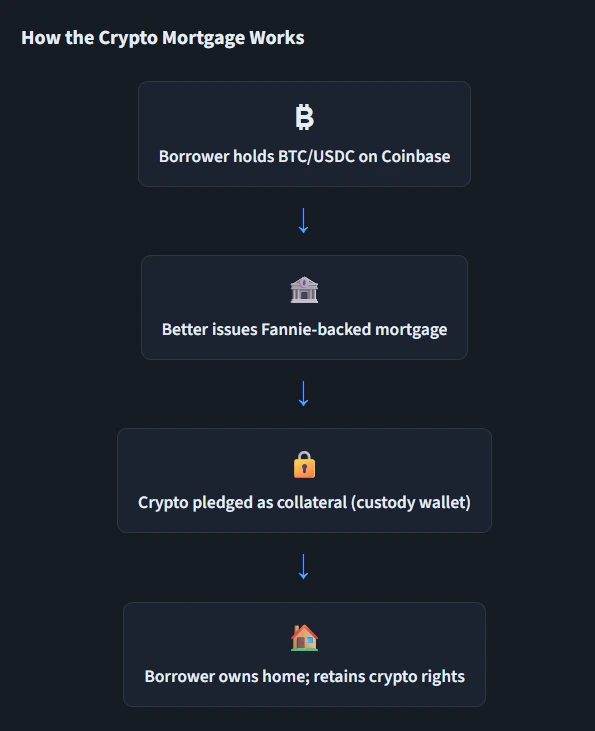

Fannie Mae has officially entered the crypto mortgage market. The government-backed housing giant now supports loans that accept digital assets as collateral. This partnership with Coinbase and Better Home & Finance marks a historic first.

The product lets homebuyers pledge Bitcoin or USDC instead of cash. Borrowers retain ownership of their crypto throughout the loan term. They also avoid triggering capital gains taxes from selling.

Key Statistics at a Glance

The FHFA Directive That Started It All

This launch traces back to a June 25, 2025, directive from FHFA Director William Pulte. He ordered Fannie Mae and Freddie Mac to accept crypto as mortgage reserves. The move aligned with the Trump administration’s pro-crypto agenda.

Under the directive, assets must sit on a U.S.-regulated centralised exchange. Borrowers do not need to convert holdings into dollars. However, a 50–60% volatility haircut applies to valuations. That means $100,000 in Bitcoin counts as just $40,000–$50,000.

Growing Demand From Younger Buyers

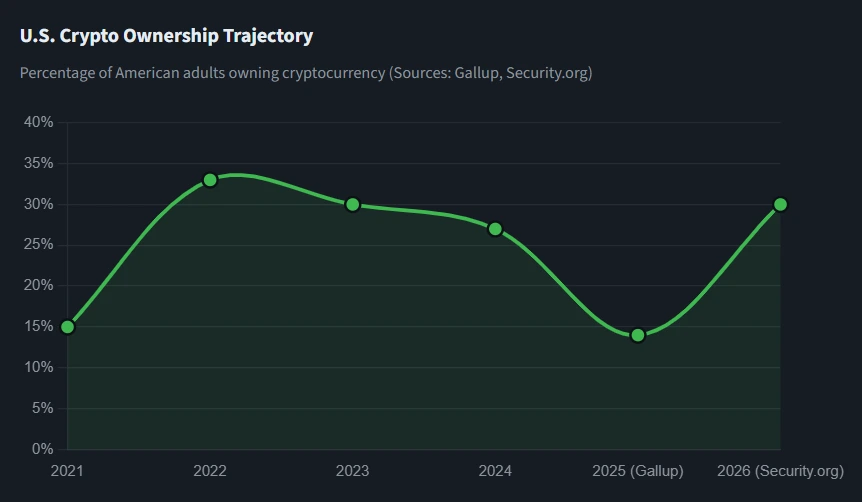

Demand for crypto-friendly mortgages is real. A Gallup survey from mid-2025 found that 14% of U.S. adults own crypto. Ownership is highest among men under 50, at 25%.

Meanwhile, a Redfin survey revealed that nearly 13% of Gen Z and millennial homebuyers sold crypto for down payments. That figure has tripled since 2019. These sales triggered taxable events that the new product eliminates.

A separate Security.org report from January 2026 pegged crypto ownership at 30% of U.S. adults. It also found 61% of current owners plan to buy more.

Risk Factors and Political Backlash

The timing carries notable risk. Bitcoin remains well below its 2025 peak. It has dropped more than 40% from its October highs. That volatility is what concerns housing regulators most.

Five Senate Democrats, led by Elizabeth Warren, sent a formal letter to Pulte. They warned that unconverted crypto assets could destabilize the housing market. The senators cited 2023 bank collapses linked to crypto.

“Expanding underwriting criteria to include unconverted cryptocurrency assets could pose risks to the stability of the housing market.”

— Senate Banking Committee Democrats, July 2025

The FHFA’s framework attempts to mitigate this. Staked assets and DeFi-locked positions are excluded. Only holdings on regulated U.S. exchanges qualify. The steep volatility haircut serves as an additional buffer.

What This Means for the Market

About 41% of American families cannot afford a standard down payment. Crypto-backed mortgages could unlock a new buyer cohort. However, the higher interest rates narrow the savings advantage.

Milo, an early mover in crypto mortgages, has financed over $65 million in deals across nine states. Newrez announced a competing program in late 2025. Fannie Mae’s entry legitimizes the entire category.

This is not a niche product anymore. The $12 trillion U.S. mortgage market now formally recognizes Bitcoin as collateral. Whether the math works for average holders remains the open question.